5 rules for creating a sound investment strategy

Rule 1 — to build wealth, start now and save for the long run

Starting young is the key to wealth accumulation and the smart way to grow your investments over time. Why is this true? Because time can have a surprisingly powerful effect on the size of your nest egg.

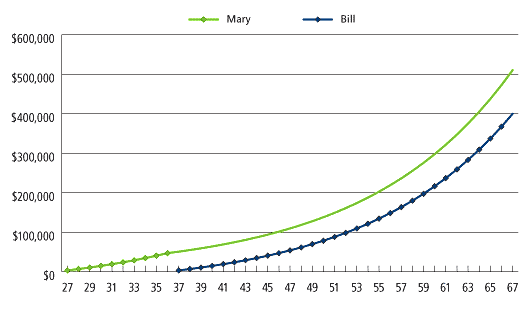

To understand how invested savings can grow over time, let's take a look at Mary and Bill's retirement plans. Mary and Bill earn the exact same salary and share identical investment goals. Their investment returns are 8% per year every year after expenses. The only difference is one starts investing earlier than the other!

Mary begins setting aside $3,000 a year in her company 401(k) at age 27. She contributes for 10 years and then stops saving completely. Bill waits until the age of 37 to start investing $3,000 a year in his 401(k), but he continues to invest for 30 consecutive years.

Starting young is the key to wealth accumulation and the smart way to grow your investments over time. Why is this true? Because time can have a surprisingly powerful effect on the size of your nest egg.

To understand how invested savings can grow over time, let's take a look at Mary and Bill's retirement plans. Mary and Bill earn the exact same salary and share identical investment goals. Their investment returns are 8% per year every year after expenses. The only difference is one starts investing earlier than the other!

Mary begins setting aside $3,000 a year in her company 401(k) at age 27. She contributes for 10 years and then stops saving completely. Bill waits until the age of 37 to start investing $3,000 a year in his 401(k), but he continues to invest for 30 consecutive years.

Mary contributed $30K in total to her retirement plan, and has $510,089 at age 67. Starting ten years later, Bill contributed $90K – three times as much! – yet by age 67 has only saved $399,640.2

Rule 2 — take advantage of the power of compounding

Rule 2 — take advantage of the power of compounding

The example in Rule #1 begins to illustrate the awesome power of compounding.

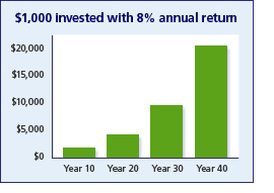

Perhaps an easier way to see how savings grow over time is to look at a one-time investment of $1,000. In this chart, you can see how just $1,000 compounds and shoots up the chart at the 10-, 20-, 30-, and 40-year marks:3

Getting a late start? You're in luck – there is help! 401(k)'s allow people who are 50 or over to contribute more than those who are younger. In 2016, a person age 50 or over can contribute $18,000 annually plus an additional "catch-up" contribution of $6,000.

Perhaps an easier way to see how savings grow over time is to look at a one-time investment of $1,000. In this chart, you can see how just $1,000 compounds and shoots up the chart at the 10-, 20-, 30-, and 40-year marks:3

Getting a late start? You're in luck – there is help! 401(k)'s allow people who are 50 or over to contribute more than those who are younger. In 2016, a person age 50 or over can contribute $18,000 annually plus an additional "catch-up" contribution of $6,000.

Rule 3 — don't let fund expenses drag you down

The expenses your fund charges can be the biggest drag on your ability to grow your nest egg.

Consider this fact: The average active U.S. mutual stock fund has an expense ratio of 1.52%.4 Let's assume that this year the stock market delivers its historical average of 10.4%. For your fund to meet the market average, your fund will need to return 11.92%.

While some may brag that their funds beat the market this year, if you deduct fund costs, this may not be true at all. This is why it's so important to be aware of your fund's expenses and look at the prospectus.

We offer index funds because they typically have low expense ratios. That's why we believe strongly in index-based investments called Exchange Traded Funds (ETFs). And for most 401(k)s, transaction fees don't apply. This helps to make ETFs very efficient investments.

To give you an idea of how low expense ratios are for index-based investments, an ETF fund (such as SPDR, series 1) tracking the S&P 500 tends to carry an expense ratio of around 0.1%. We call that a market-efficient fund!

Consider this fact: The average active U.S. mutual stock fund has an expense ratio of 1.52%.4 Let's assume that this year the stock market delivers its historical average of 10.4%. For your fund to meet the market average, your fund will need to return 11.92%.

While some may brag that their funds beat the market this year, if you deduct fund costs, this may not be true at all. This is why it's so important to be aware of your fund's expenses and look at the prospectus.

We offer index funds because they typically have low expense ratios. That's why we believe strongly in index-based investments called Exchange Traded Funds (ETFs). And for most 401(k)s, transaction fees don't apply. This helps to make ETFs very efficient investments.

To give you an idea of how low expense ratios are for index-based investments, an ETF fund (such as SPDR, series 1) tracking the S&P 500 tends to carry an expense ratio of around 0.1%. We call that a market-efficient fund!

Rule 4 — use diversification to balance risk and return

The concept of diversification is both easy to understand and extremely important.

There are three main asset classes: stocks, bonds, and cash. Owning any single stock or bond is more risky than owning many stocks or bonds. To diversify within an asset class, simply own many securities – not just a few.

Then consider the different asset classes you can choose from. Stocks, as an asset class, are the most volatile but have had the greatest returns over time. Bonds and cash follow. Because financial markets prosper or struggle, depending on economic circumstances, there is no guarantee of high future returns. Even wide diversification can't fully protect you against a declining market.

But there's good news. Stocks and bonds do not always move together in lockstep and their volatility often differs. Therefore, holding a broad-based portfolio of different asset classes gives you wide diversification that can help to limit your risk.

Thus, there are two key rules to follow:

There are three main asset classes: stocks, bonds, and cash. Owning any single stock or bond is more risky than owning many stocks or bonds. To diversify within an asset class, simply own many securities – not just a few.

Then consider the different asset classes you can choose from. Stocks, as an asset class, are the most volatile but have had the greatest returns over time. Bonds and cash follow. Because financial markets prosper or struggle, depending on economic circumstances, there is no guarantee of high future returns. Even wide diversification can't fully protect you against a declining market.

But there's good news. Stocks and bonds do not always move together in lockstep and their volatility often differs. Therefore, holding a broad-based portfolio of different asset classes gives you wide diversification that can help to limit your risk.

Thus, there are two key rules to follow:

- Diversify within each asset class. Don't hold just one or two stocks. The risk is high that you will lose money versus a small chance that you will outperform the markets. Instead, choose an index fund or broad-based fund that covers a large swath of the market. Example: A diversified stock portfolio might include a 80% investment in a total U.S. market index fund and a 20% investment in a total international stock market fund.

- Diversify across asset classes. This means you should choose to invest a percentage of your savings in each of the asset classes – stock, bonds, and cash – based on your personal comfort level. Example: A person who's 40, with a moderate tolerance for risk, might allocate 70% to stocks and 30% to bonds in their 401(k), and manage cash reserves in their personal money market account.

Rule 5 — make sure your assets are allocated correctly

Asset allocation is technically just part of the diversification strategy discussed above. The important thing to know is that since the first asset allocation study was conducted in 1986, industry research and financial theory have continued to demonstrate that asset allocation has a greater influence on your portfolio's performance than the specific funds you select.5

The important point is that you should really consider a percent to invest in each asset class (e.g. 60% stocks, 40% bonds). Your asset allocation needs to fit your goals, your comfort with market swings, and the time until you will use those funds.

The younger you are, the more time you have to travel through the market's ups and downs. A younger person should consider investing more in stocks – upwards of 90% if she is in her mid-twenties – with only 10% in bonds.

Conversely, a person who is 62 and plans on retiring in three years may be better served by a portfolio comprised of 60% in stocks and 40% in bonds. In general, most people want to keep more of their investments in stocks, given the asset class's long-term history of superior performance. Even at age 65 you may not have to access your stock funds for ten or twenty years or more, which means you may have a good chance of riding out storms in the market.

With a good asset allocation plan, you can invest with confidence. Some providers offer tools like auto-rebalancing at no additional charge. They will automatically maintain the percent allocation you designate, making it easy to manage your plan.

The important point is that you should really consider a percent to invest in each asset class (e.g. 60% stocks, 40% bonds). Your asset allocation needs to fit your goals, your comfort with market swings, and the time until you will use those funds.

The younger you are, the more time you have to travel through the market's ups and downs. A younger person should consider investing more in stocks – upwards of 90% if she is in her mid-twenties – with only 10% in bonds.

Conversely, a person who is 62 and plans on retiring in three years may be better served by a portfolio comprised of 60% in stocks and 40% in bonds. In general, most people want to keep more of their investments in stocks, given the asset class's long-term history of superior performance. Even at age 65 you may not have to access your stock funds for ten or twenty years or more, which means you may have a good chance of riding out storms in the market.

With a good asset allocation plan, you can invest with confidence. Some providers offer tools like auto-rebalancing at no additional charge. They will automatically maintain the percent allocation you designate, making it easy to manage your plan.

Summary

Keys to creating a sound investment strategy

By following these rules you can feel confident that you're building a solid investment plan for the long term. Stick with your strategy, avoid the performance-chasing mentality, and you stand a great chance of weathering the inevitable storms.

- Start investing now

- Time is your friend – compounding can be huge

- High costs are a drag on profits – avoid them

- Diversify, diversify, diversify

- Manage asset allocation carefully

By following these rules you can feel confident that you're building a solid investment plan for the long term. Stick with your strategy, avoid the performance-chasing mentality, and you stand a great chance of weathering the inevitable storms.